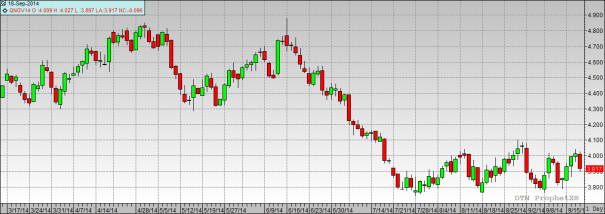

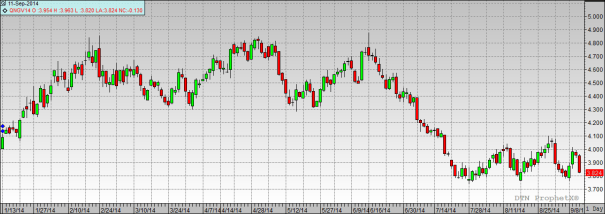

For the 23rd week in a row – the Natural Gas Storage Report has shown a build up of gas in storage greater than the 5-year average for the corresponding week. This means we should continue to see gas prices remaining within the narrow trading range of $3.75 – $4.10.

This week’s report also exceeded the analyst’s expectations as well. The poll by the Wall Street Journal showed the experts were looking for an increase of 92 bcf. The report surprised most showing an increase of 97 bcf. Last year the increase for this week was 82 bcf and the corresponding 5-year average was 71 bcf.

The natural gas in storage this year is now only 386 bcf lower than than last year. Fears of not having enough gas in storage to meet the country’s needs this winter continue to subside. Prices for gas and electricity should remain fairly steady until we see what our winter weather provides us this year.