Last month BP (NYSE: BP) released the Statistical Review of World Energy 2014. This report is one of the most comprehensive sources of global and country level statistics on production and consumption of oil, natural gas, coal, nuclear power and renewables. Right after the release of the report, I wrote a short post discussing the highlights. Today I will take a deeper dive into oil production and consumption figures. In coming weeks, I will delve into the rest of the report.

Oil Production

First a note about BP’s definitions. “Oil” in the BP Statistical Review (BPSR) is defined as ”crude oil, tight oil, oil sands and natural gas liquids”, but excludes biofuels and liquid fuels produced from coal or natural gas. Consumption numbers do include all liquid fuels, so consumption numbers are always greater than production numbers, but this is merely an artifact of BP’s definitions.

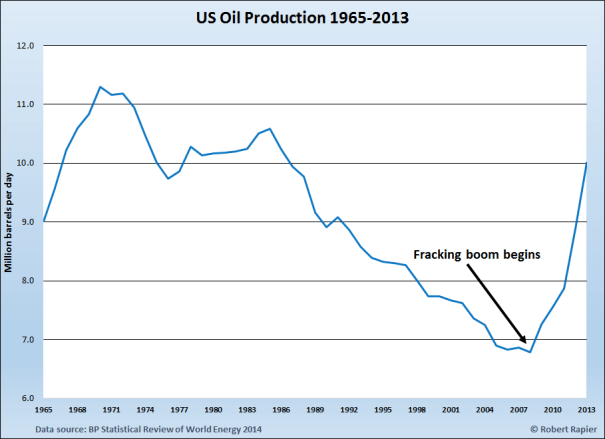

Global oil production advanced in 2013 by 557,000 barrels per day (bpd), reaching a new all-time high of 86.8 million bpd (an increase of 0.6 percent over 2012). After declining in 2009, global crude oil production has now increased 4 years in a row. But as I noted in last month’s short article, while global oil production did indeed set a new record, the US production increase alone was 1.1 million bpd. Thus, outside the US global production actually declined by 554,000 bpd.

The 1.1 million bpd gain in US oil production was the largest year over year gain for any country in 2013, and the largest gain in US history. For perspective, the second-largest increase in oil production was recorded by the United Arab Emirates with a gain of 248,000 bpd over 2012, and Canada was the only other country in the world to record an increase of more than 200,000 bpd, at 208,000 bpd over 2012. The US remained the world’s third-largest oil producer at 10 million bpd in 2013, trailing Saudi Arabia’s 11.5 million bpd and Russia’s 10.8 million bpd. Rounding out the top five were China (4.2 million bpd) and Canada (3.9 million bpd).

Just to put the current US oil boom into further perspective, over the past five years global oil production has increased by 3.85 million bpd. During that same time span, US production increased by 3.22 million bpd — 83.6 percent of the total global increase. Had the US shale oil boom never happened and US production continued to decline as it had for nearly 40 years prior to 2008, the global price of oil might easily be at $150 to $200 a barrel by now. Without those additional barrels on the market from (primarily) North Dakota and Texas, the price of crude would have risen until supply and demand were in balance.

Libya had the largest decline of any country due to military action there. Oil production fell in Libya by 521,000 bpd, a 35 percent loss from 2012. Production in Iran was down nearly 200,000 bpd, while military action also impacted Syria’s production, which fell 115,000 bpd. Production in Saudi Arabia and Nigeria was down about 100,000 bpd from 2012.

Oil Consumption

Oil accounted for 33 percent of all the energy consumed in the world in 2013. Globally, oil demand increased by 1.4 million bpd over 2012 to 91.3 million bpd, keeping upward pressure on crude prices throughout the year. After two years of declines, US consumption increased by 397,000 bpd – a 2 percent increase from 2012. While much has been made of a slowdown in China, oil demand there still increased by 390,000 bpd (following a 500,000 bpd increase from 2011-2012). Despite the slowdown in the rate of growth from the previous year, this represented a 3.8 percent consumption increase for China, 2.5 times the global increase of 1.4 percent.

Together the US and China were responsible for 56 percent of the global increase in oil demand in 2013. The big difference between the two countries is that US oil production was up far in excess of our increase in consumption, while oil production in China edged up by only 24,000 bpd. This means that while US oil imports declined and finished product exports (e.g., gasoline, diesel, jet fuel) increased, China’s dependence on oil imports continued to increase.

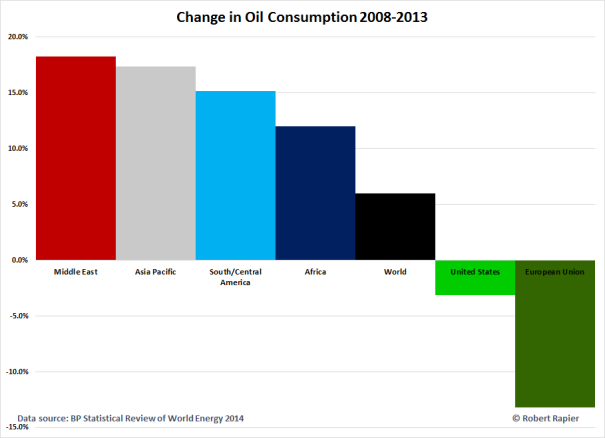

Double-digit percentage increases in oil consumption were recorded by Pakistan, Venezuela, and Azerbaijan from 2012 to 2013, and over the past five years double-digit percentage consumption increases were recorded by Central and South America (15.2 percent), the Middle East (18.3 percent), Africa (12 percent), Asia Pacific (17.4 percent), and the former Soviet Union (12.8 percent). Oil demand in the developed countries belonging to the Organisation for Economic Co-operation and Development (OECD) decreased 5.3 percent over the past five years, while demand in non-OECD countries increased 20.3 percent.

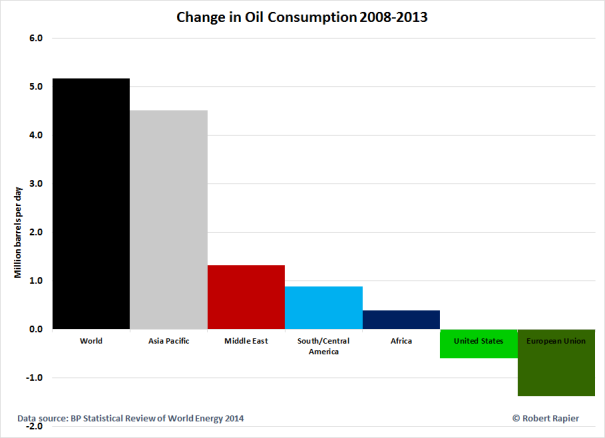

After posting the above graphic to my Twitter feed, several asked if I would reproduce it in barrels per day. I have to agree that this really puts Asia Pacific’s influence on global oil demand growth in perspective. Over the past 5 years, 87 percent of the demand growth for oil came from the Asia Pacific region:

Oil Prices

The loss of oil production from Libya and strong demand in developing countries ensured that oil prices remained high, despite surging US production. Contrary to expectations — given a tighter supply/demand picture for international crudes — Brent crude declined by $3.01 from 2012 to a yearly average of $108.66/bbl. Prices for West Texas Intermediate (WTI), on the other hand, actually averaged $97.99/bbl for the year, an increase of $3.87/bbl from 2012.

Conclusions

The story of oil in 2013 was one of surging US production and increasing demand in developing countries. The US continues to lead the world in increasing oil production, while developing countries — in particular the Asia Pacific region — have added the vast majority of oil demand in recent years. Arguably the only thing preventing the world from experiencing oil prices in the $150-$200/bbl range is the continuing shale oil boom in the US.

Link to Original Article: World Sets New Oil Production and Consumption Records